Economic Benefit (Traditional) Split Dollar Arrangement

There are two types of economic benefit arrangements: endorsement and collateral assignment:

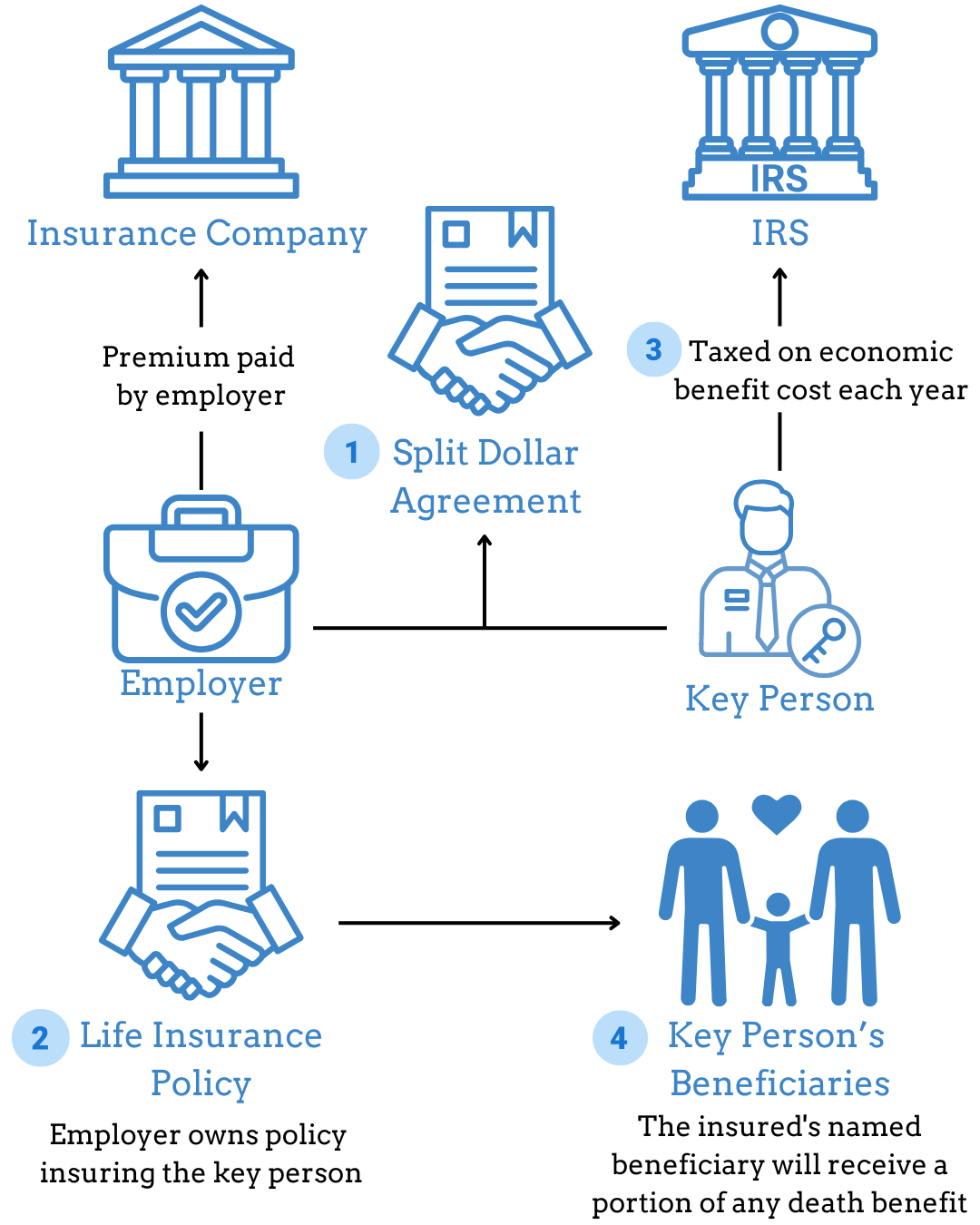

Endorsement Arrangement: The employer owns the policy but allows the key person to name the beneficiary of a portion of the policy death proceeds. The employer retains all other rights to the policy.

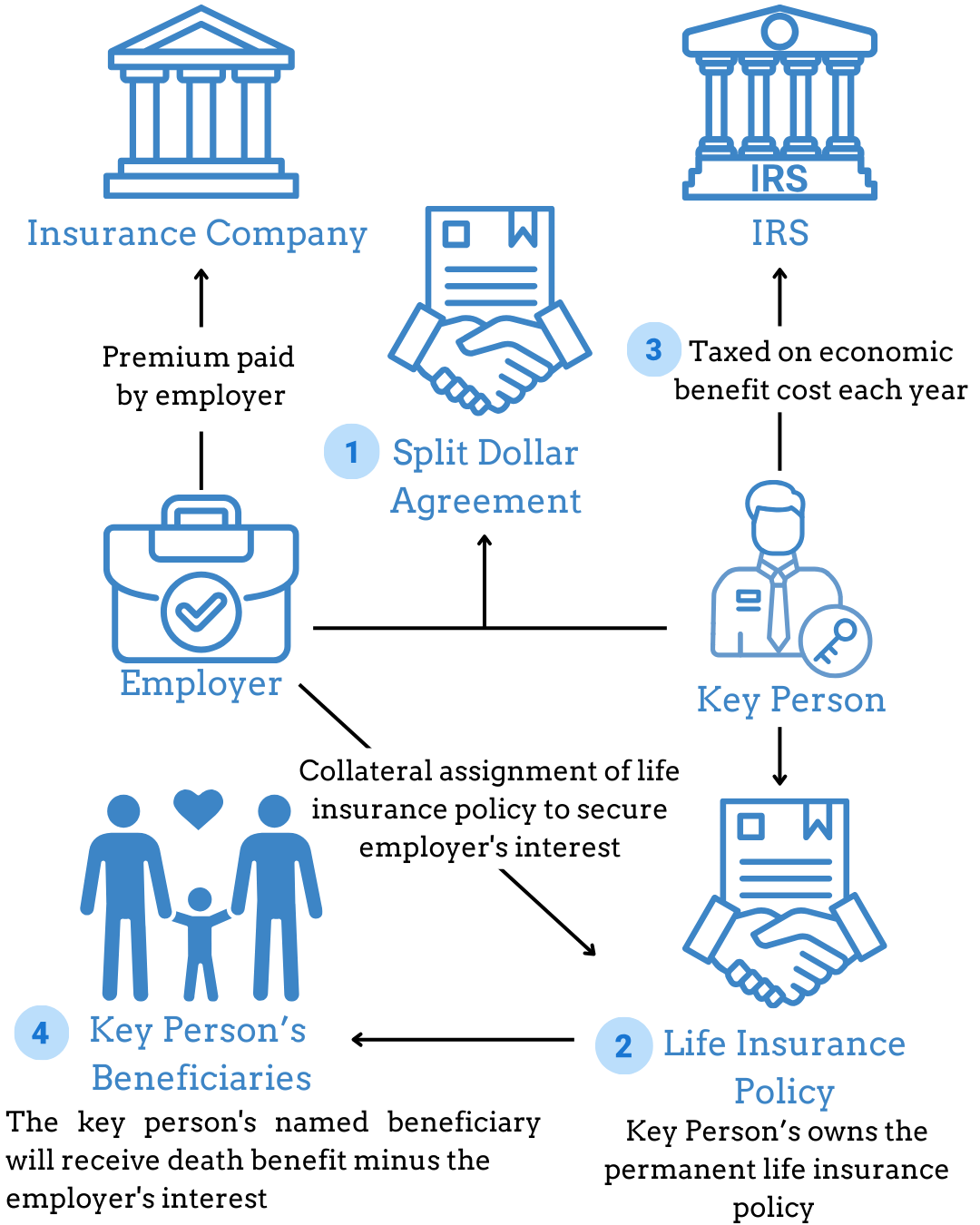

Collateral Assignment Arrangement: The key person owns the policy but the employer "owns" all of the policy cash value. This is often referred to as a "non-equity" arrangement.

Both types have the same tax consequences:

The employer owns the policy when using the endorsement arrangement.

The key person’s rights are limited.

The key person is taxed on the economic benefit cost under both arrangements.

ECONOMIC BENEFIT (ENDORSEMENT METHOD) SPLIT DOLLAR ARRANGEMENT

Whatever it is, the way you tell your story online can make all the difference.

ECONOMIC BENEFIT (COLLATERAL ASSIGNMENT) SPLIT DOLLAR ARRANGEMENT

Whatever it is, the way you tell your story online can make all the difference.

How to Exit or Roll out of an Economic Benefit (Endorsement or Collateral Assignment) Split Dollar Arrangement

Endorsement Plan

Employer Keeps the Policy

When the arrangement terminates, no transfer of the policy is required. The employer as policyowner may keep or surrender it as best suits future employer goals.

Collateral Assignment Plan

If the arrangement is a collateral assignment, the employer via the collateral assignment can take over the policy (making themselves the owner of the policy) or do the following options:

Employer Transfers the Policy to Insured

The policy can be "rolled out" to the key person. Their position as key person or stockholder will affect how the ownership change is treated. For example, when a key person retires, the employer may owe the key person money under a deferred compensation agreement, in which the policy might be transferred in satisfaction of that deferred compensation obligation.

A generous employer might choose to transfer the policy to the key person even if there is no deferred compensation arrangement. In either case, the key person would pay tax on the fair market value of the policy at that time, and the company would receive an offsetting deduction.

Employer Sells the Policy to the Insured

The employer may agree to sell the policy to the insured for a cash payment or a note payable equal to the employer’s cash value interest.

Death Benefit

In the event the key person dies while an arrangement is still in place, the terms under the split dollar agreement would determine the amount paid to the employer and the death benefit payable to the named beneficiaries.

How the IRS Looks at Split Dollar Arrangements

During the arrangement, the key person has the right to name the beneficiary of a portion of the death benefit. The key person has no interest in the cash value.

The IRS regulations provide that the key person receives a taxable economic benefit each year—namely the insurance protection—since the employer paid all of the premiums.

The key person is taxed on the value of insurance protection each year. The taxable value of the annual insurance coverage (measured in dollars per $1000 of coverage) is based on an IRS table or the insurance company’s applicable one-year term insurance rates.

As a key person ages, the cost of coverage increases for the same amount of death benefit.

If the arrangement terminates while the key person is still alive, the employer keeps the policy. The key person has no rights in the contract but is no longer taxed.