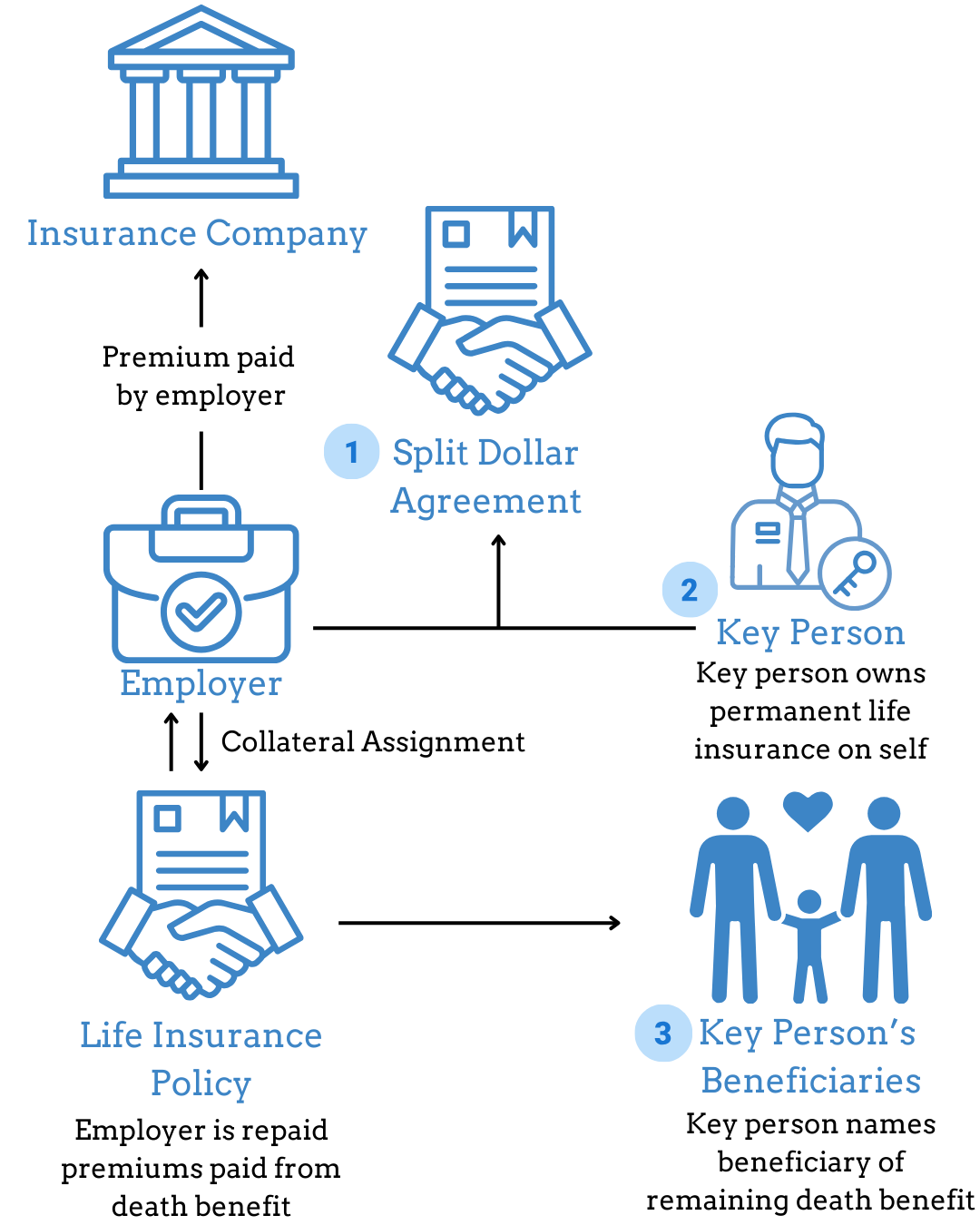

Loan Regime(Collateral Assignment) Split Dollar Arrangement

If an employer wants the key person to accumulate equity in the life insurance policy, the parties may agree to implement a split dollar loan arrangement.

Under this arrangement, the key person owns a permanent life insurance policy. The arrangement treats each premium payment made by the employer as a loan to the key person. In exchange for the loan, the employer has a collateral assignment against the policy to ensure recovery of the loan principal. As the cash value of the policy grows, the key person owns the difference between the policy cash value and the amount of the loan. If loan interest is forgiven by the employer, the key person pays income tax on the forgiven amount. A second option is for the loan interest to accrue.

The key person owns the policy and names the beneficiary.

The employer’s rights are limited to repayment of the loan principal.

Loan arrangement taxation can vary depending on whether the loan is forgiven or repaid.

LOAN REGIME (COLLATERAL ASSIGNMENT) SPLIT DOLLAR ARRANGEMENT

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

How to Exit or Roll out of a Loan Regime (Collateral Assignment) Split Dollar Arrangement

Forgiveness of the Loan

For loan arrangements, the key person owns the contract but owes the employer upon termination of the split dollar agreement, which typically occurs at the key person’s retirement. The employer could forgive the outstanding loan balance, in which case the key person would pay taxes on the amount of the loan forgiven. The company would receive an offsetting deduction. Since the key person is now the owner of the policy, they can use a withdrawal from the policy or outside funds to pay the taxes due.

Repayment of the Loan

The insured can repay the employer using cash or other out-of-pocket assets outside of the policy.

Death Benefit

In the event the key person dies while an arrangement is still in place, the split dollar agreement would determine the amount to be paid to the employer, with the remainder of the death benefit payable to the named beneficiaries.

How the IRS Looks at Split Dollar Arrangements

Loan Regime (Collateral Assignment) Split Dollar Arrangement (Key Person Owns Policy)

During the arrangement, the employer pays premiums directly to the insurance company. Each premium payment is treated and documented as a loan to the key person.

The Internal Revenue Code requires that interest be accounted for in any employer provided loan arrangement. Interest must either be paid or accrued and added to the loan balance, or the employee must be taxed on the value of the interest they were not required to pay.

The loan can either be structured as a term loan or as a demand loan (meaning the employer can call the loan at any time). Loans with a certain duration generally use the Applicable Federal Rate (AFR) appropriate to that term (short-, mid-, or long-term), while demand loans use a blended short-term federal rate.

Loan arrangements can be structured in many ways—for example, with accrued interest or interest paid each year. Employer provided split dollar loans are generally provided with a below market interest rate, including zero percent. The employee is taxed annually on the difference between the interest that would have been paid at market rates versus the amount the employee was actually required to pay.

If the employer receives interest from the key person, the employer is taxed on that amount.

The employer’s interest in the life insurance policy is secured with a collateral assignment. The collateral assignment ensures that significant rights in the policy remain with the employer while the split dollar arrangement is in place.